Real estate investors may need to test every property for meth.

There may be a need now to test every home before you purchase it for meth…or end up with a huge bill or lawsuit. Most self tests cost around $30 to check if meth was used in a home, a lot cheaper than remediation or a lawyer.

We will see where this flipper (the seller) ends up and what it will cost them.

https://thecashflowmortgagecompany.com/wp-content/uploads/2019/09/architecture-beautiful-exterior-106399-1.jpg14402160Jenna Weldonhttps://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svgJenna Weldon2020-07-20 11:00:382020-07-20 11:00:38Real estate investors may need to test every property for meth.

Check out this cozy little hold-and-rent property our client purchased Greeley, Colorado! This deal was funded using a Hard Money Mike loan.

We love seeing our clients’ success stories and look forward to checking in on the progress with their investments.

Ready to fund your own investment property deal? Chances are good that we can help!

Hard Money Mike is a lender based in Colorado. We regularly lend money on all types of commercial-based properties. So whether you have your eye on a potential fix-and-flip, vacant land, whole tailing, or a builder bridge loans, we’re happy to help make your investment property dreams come true.

We even lend on deals in several states outside of Colorado, so don’t let our location stop you from achieving your investment goals. If we’re not yet lending in your state, we’re still happy to discuss your numbers and plans with you to make sure you’re on the right track.

In the market for a property in the single-family or commercial sector? Our sister company The Cash Flow Mortgage Company funds investor loans on those, too! We’ve got a lending solution to most investment opportunities, so let’s get you on the path to investment property greatness.

Questions or just need help deciphering your numbers? Feel free to reach out!

Hard Money Mike 303-539-3000

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

Rates on the conventional side have maintained strong with rates in the low 3’s. If you’re still wondering whether or not you should refinance, we’re going to dive into what we call ‘The Tipping Point Rate.’

This week, we’re seeing more larger non-conventional companies dipping their toes back into the investor loan water. This gentle ease back in helps increase liquidity, but it still comes at a price: Lower LTVs and higher costs.

What This Means for You:

There is an exact rate where it’s wise to refinance. We call this ‘The Tipping Point Rate.’ This specific rate is the point where you won’t pay a penny more in principal and interest over the life of the loan.

Going above this point might increase your cash flow, but it will end up costing you more in the long run. Sometimes this means it’s better to stick with what you have now. We’re focused on putting more money in your pocket and less in the bank’s pocket.

This is for investors looking to increase monthly cash flow without adding lifetime cost of debt. So, if you’re solely concerned about your monthly cash flow, this probably isn’t the program for you.

So how does this work? Let’s take a look at an example.

Joe is an investor who is looking at refinancing to increase his cash flow every month. But not if it means paying tens of thousands of dollars extra to the bank in principal and interest.

Joe has been paying his current mortgage for 5 years. If he keeps the loan until it’s paid in full, he’ll end up paying $360k in payments over the next 25 years.

Joe wants to know the exact rate that he can refinance to a new 30-year fixed without increasing his amount owed. If it exceeds $360k, then he won’t refinance.

By knowing this exact rate, he can stretch his payments out and lower his interest rate without paying a penny more over the life of the loan.

How do we find Joe’s Tipping Point Rate?

Luckily, we have a handy program that can calculate just that. If you would like to know your own Tipping Point Rate, send us an email! We’ll run the report specifically for you and your property!

Note: The Cash Flow Mortgage Company doesn’t currently lend in all states, but we are always happy to help and make sure you understand your numbers!

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

Check out these inspiring Before-and- After property transformation photos! These pics come courtesy of one of our clients’ fix-and-flip projects in Canal Winchester, OH!

When you go through Hard Money Mike, you can count on a hassle-free process for rehab projects like this one. Hard Money Mike is a lender based in Colorado, lending money to several states, including Ohio. We regularly lend money on all types of commercial based properties: fix and flip, land, whole tailing, and bridge loans. So regardless of what type of property transformation you’re trying to achieve, chances are, we can help you fund the deal!

Call Mike Bonn at 303-539-3000 or email Mike@HardMoneyMike.com

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349*

We might be based in Colorado, but that doesn’t mean that as our client you have to miss out on deals in other states! In fact, Hard Money Mike lends on properties in several states, like with this Texas fix-and-flip!

Texas fix-and-flip deal

We love seeing our clients crush their investment goals, even from afar! Take, for instance, this Texas fix-and-flip property purchased by one of our clients. We were able to fund this deal in a week.

Yes, you read that right.

Investors and wholesalers alike will find the short-term loan process at Hard Money Mike quick and easy. We pride ourselves on making it easier to get the cash flow you need for quick property purchases. Who wants to wait around when they’re trying to close a deal and add to their investment portfolio?

In other words, we want to help you make more money even faster!

Hard Money Mike is a lender based in Colorado, lending money on all types of commercial based properties: fix and flip, land, whole tailing, and builder bridge loans.

Have your eyes set on an investment property on the single-family or commercial building side? The Cash Flow Mortgage Company funds investor loans on properties in both of these categories. Long story short: whatever deal you’re trying to fund, chances are, we can help you get it done!

Give us a call:

Hard Money Mike 303-539-3000

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

The markets are stabilizing, and underwriting term times are back in pre-Covid standards.

With rates for single-family investor properties on conforming loans hovering around the low 3’s, it might be time to look at locking in and increasing your cash flow.

What This Means for You:

As an investor, there is money in the money—Your money!

Your credit score is the key to keeping more of your money. No matter your income situation, the better your score, the cheaper the money. Cheaper money equals more cash in your pocket.

How to raise your score and increase your cash and cash flow

Do you want to keep money in your life or keep supporting a banker’s life? We’re pretty sure we know the answer to that particular question.

They say that Vegas was not built on the gambler’s winnings. The same can be said about banks. Banks keep popping up everywhere, even when most banking has gone online.

Why is that? Because they know there’s money in your money.

So how can you better prepare your credit score for an investor loan?

Plan before you apply by checking your score online.

Stop applying for ANY credit at least 60 days before a loan application.

Raise your score with one or two of these simple methods:

Use private money when you can and keep it off your credit. If you can borrow from a private individual or entity that doesn’t report on credit to pay off/down your credit, do it BEFORE your next statement date.

Don’t close paid off accounts.

Pay down your credit cards before due dates. This will take extra cash now, but it will save you tens of millions in the future.

Keep balances below 30% of outstanding balances on revolving accounts like credit cards.

Dispute any item that should not be on your report.

This list does not include paying your accounts on time. That’s a no-brainer. You should always pay on time. There’s typically no quick fix for late payments.

Stay tuned, because next up, we’ll be covering how to check your credit on your own! In the meantime, if you have questions about your score, what it’s costing you, or what a better score could save you, reach out! We’re always happy to go over the numbers with you!

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

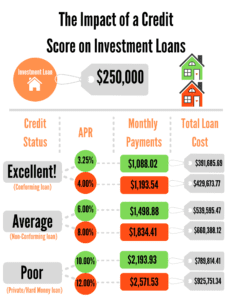

How much money might a lackluster credit score be costing you over the life of your investment business?

You probably hear a lot of talk in the mortgage industry about your credit score and the effect it can have on your interest rates, but do you really have an idea of how much it’s affecting your bottom dollar?

Do you know how to determine your Return on Credit (ROC)?

Can you crunch the numbers to figure out how much your score is helping your cash-flow (or how much money it’s sucking out every month?)

These calculations can get complicated, but the takeaway here is that a less-than-stellar score can really be costing your tens of thousands of dollars over the lifetime of your loan. And when your loan is on an investment property, (or several,) you may as well be lighting your profits on fire.

We want to help! Contact our team so we can help you see where you’re currently at, and where you could be going instead.

Let’s get you to your goals faster by trimming some of the fat from your financing!

Hard Money Mike is a lender based in Colorado offering services in several states. We lend money for all varieties of commercial-based properties. So whether you’re trying to finance a fix-and-flip, vacant land, whole-tailing, or looking for a builder bridge loan, we’ve got you covered.

Call Mike Bonn at: 303-539-3000 or email Mike@HardMoneyMike.com

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

https://thecashflowmortgagecompany.com/wp-content/uploads/2020/06/jp-valery-mQTTDA_kY_8-unsplash-scaled.jpg17072560Mike Bhttps://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svgMike B2020-06-08 09:55:222020-06-11 10:55:59What’s the Cost of Your Credit Score?

For some of you, they do. For others, you might be left thinking, “But wait! What if I’m not going to keep the property for 24 or 30 years?At what point does it actually make sense to refinance?”

However, if you are not going to keep the property through the next 30 years, you’ll need to look hard at what the costs will be over the expected period. The key here is determining which path will cost you more money and which one will keep more in your pocket.

GOAL: Keep more money in your life and less in the hands of bankers.

Let’s look at an example:

You’re planning to keep a property for 3 years and then sell it. The question is, what will put more money in your pocket and cost you the least over those next 3 years?

Here is how we figure this out:

Step 1: Ask your mortgage company to run an amortization chart on your current loan and your new loan.

2: Then, pull your principal and interest from your current mortgage company’s website.

3: Next, ask your mortgage broker to give you the principal and interest from the new loan.

4: On each loan, multiply the payments by 36 (the 3-year window before you sell the property) and add the balance of your loan at the end of 3 years.

5. Lastly, compare notes and find out what would be the lowest amount. This is the one that will keep more money in your pocket.

Ultimately, this is just a pure and simple scenario of determining exactly how much the loan will take out of your pocket over the course of 3 years. We’re not looking at monthly cash flow, because true dollars out are pure and simple. This is your true cost out of your pocket.

If you need help, we’re happy to step in. Give us a call, and we can run all the numbers for you and see if it makes sense. If it does, we can help you out even further by securing low rates and costs on your refi!

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

https://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svg00Mike Bhttps://thecashflowmortgagecompany.com/wp-content/uploads/2021/03/TheCashFlowMortageCompany-logo.svgMike B2020-06-05 12:14:522020-06-11 10:56:33How to Know When a ReFi Makes Sense

We’re so impressed with this Multi-Unit Fix-and-Flip in Ohio!

While we’ve seen a good share of motivating investor inspo over the past few weeks, we never get tired of seeing the incredible transformations from our clients. Check out these awesome Before-and-After photos of a multi-unit fix-and-flip from one of our clients in Columbus, Ohio!

While seeing these awesome before-and-afters is certainly inspiring, it also requires some cash to pull off similar results. If you’re looking for ways to fund your future fix-and-flips, we have a solution for you!

Hard Money Mike is a lender based in Colorado. We lend money on all types of commercial-based properties. So whether your dream deal is a fix-and-flip, vacant land, whole-tailing, or requires a builder bridge loan, we’ve got you covered. We offer services in several states, including Ohio.

Call Mike Bonn at: 303-539-3000 or email Mike@HardMoneyMike.com

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

Thankfully, it’s looking like another great week for standard conventional mortgage rates.

So far this week, all evidence is pointing towards increasing stability and improvements on the conventional mortgage front.

Depending on whether you pay your mortgage person points or you have them wrapped into your loan, rates fluctuate between low 3’s and low 4’s.

We’re seeing great rates on the conforming side.

Every week, the non-traditional loans are reappearing with increased frequency.

Some lenders have decreased credit score requirements to 680.

Rates are still on average above 7%, but signs are showing that they will drop soon.

LTVs are inching higher, but not to the degree we have seen them in the past.

In short: conventional mortgage interest rates are really good. But what does that mean for you?

How do you know when it’s smart to refinance your rental (or any) property?

Let’s face it: as rates drop, the question of whether or not to refinance runs through all our minds.

Would you like to find out (without the sales pitch from your mortgage person?)

Anyone can crunch the numbers in just a few minutes with just a few items.

Yes. It involves math. But we swear it’s EASY.

For now, all you need is a piece a paper, a pen, a calculator, and your mortgage information. (You can pull this info directly from your mortgage company’s website). Then, follow these three steps:

Step 1: Locate the amount you pay monthly for principal and interest. (Ignore everything but your principal and interest (i.e. taxes and insurance).

Step 2: Locate the number of months remaining on your loan.

Step 3: Multiply your monthly payment by the number of months you have left on your loan.

That’s it!

Let’s look at an example:

A: Your monthly principal and interest payment is $1,200.

B: You have 288 payments left on your loan.

C: $1,200.00 X 288 = $345,600

(Scary sometimes to see how much you really owe, isn’t it? Don’t panic.)

Now, let’s say that you have an opportunity to refinance and lower your interest rate with a new payment of $1,100. Should you do it?

Let’s take a look:

On your new loan, you’d pay $1,100.00 for 30 years (or 360 months). That’s $1,100.00 x 360 = $396,000.00

If you refinance, you’d increase your monthly cash flow $100.00. However, as a result, you’d pay an extra $50,400.00 over the life of your loan!

So, is the extra $100/month worth an extra 72 months (6 years) of mortgage payments? Does refinancing make sense for you financially? Well, that’s up to you.

Perhaps cash flow is more important at this time in your business life and paying the extra years is ok with you. That’s a decision only you can make. At least when you know all the numbers, you can make your call an educated one.

Try it on all your loans and find out what makes sense for you!

Your payments __________________ Months remaining _______________

Total remaining to be paid ___________________

Okay, we’re sure a few questions are swimming around in your head, so we’ll see if we can answer some of the most common ones upfront:

Q: “What if I’m not going to keep the property for 24 or 30 years? At what point does it make sense to refinance?”

A: That’s coming up in the next article.

Q: “What if I want to use those savings and pay down my mortgage?”

A: We’ll be addressing that in a future article as well.

Q: “What is my breakeven interest rate?”

A: There are so many paths you can go down and we’ll cover as many as we can. We’ll also provide a tool for you to run all these scenarios.

Today, it’s all about knowing your raw numbers.

Want an investor tool that can run these numbers (plus your breakeven rate and many more) in seconds? We have one in the works. Just get on our contact list, and we’ll let you know when it’s ready!

By knowing these numbers, you can save tens of thousands on each refinance.

Don’t feel like doing this or worry the math might overwhelm you? No worries! Shoot us an email with your current statement and we can run them for you.

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.